By John Adams, Principal and Head of Investment Banking

- Net Income Improves From the Previous Quarter Due to Lower Provision Expense

- Net Income Declines from a Year Ago Because of Lower Net Interest Income

- Net Interest Margin Falls to Historic Low

- Deposit Growth Normalizes after 2Q PPP, Stimulus Boost

- Asset Quality Metrics Show Modest Deterioration

- Industry Reports Strong Capital and Liquidity

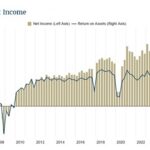

During the three months ending September 30, quarterly net income for the 5,033 FDIC-insured commercial banks and savings institutions that filed Call Reports totaled $51.2 billion, up $32.4 billion (173%) from the second quarter of 2020 but down $6.2 billion (10.7%) from the year-ago quarter. The quarterly increase in net income was attributable to a $47.5 billion (76.8%) decline in provision expenses between the second and third quarter 2020. Lower net interest income drove the annual decline in net income. Slightly more than half (51.3%) of all banks reported lower net income compared to a year ago, and the share of unprofitable institutions increased to 4.7%. The return on assets decreased to 0.97% from 1.25% in the third quarter of 2019, but was up from 0.36% in the second quarter of 2020.

The number of FDIC-insured commercial banks and savings institutions reporting declined from 5,066 to 5,033 during the third quarter of 2020. One new bank was added, 33 institutions were absorbed by mergers, and no banks failed. The number of institutions on the FDIC’s “Problem Bank List” increased to 56 from 52 last quarter. Total assets of problem banks increased from $48.1 billion to $53.9 billion.