Market Approach

Each of the three major U.S. stock indexes notched a record high in 2025, although softening during the last week of December, hurtling past tariffs, a government shutdown and fears of a bubble in artificial intelligence. Analysts attributed the continued rise of share prices during 2025 to overlapping trends: resilient corporate earnings, a series of interest rate cuts by the Federal Reserve meant to boost hiring and a near inexhaustible enthusiasm for artificial intelligence. Artificial intelligence has been the defining force driving the market for the last three years. In 2023, the S&P 500 surged 24%, after the debut of ChatGPT the prior year unleashed a fervor around the companies most likely to benefit from a technological revolution that harkens back to the dawn of the internet. In 2024, the broad market index rallied another 23%.

Tariffs, which threatened to derail markets in the spring, eased into an afterthought over the latter half of the year. A day after tariffs were announced on April 2, major stock indexes shed about $3.1 trillion in value. The selloff amounted to the biggest one-day decline in markets since the onset of the COVID-19 pandemic. Days later, a major swathe of the tariffs were suspended, sending the market to one of its largest ever single-day increases. Even as markets proved resilient, the gains during 2025 remained concentrated in a handful of tech giants, known as the magnificent seven: Alphabet, Amazon, Apple, Meta, Microsoft, Tesla and Nvidia. In September, worries over AI threw cold water on those stocks, causing their prices to waver, but in November, blockbuster earnings from Nvidia helped rebuke AI fears and shake markets out of the doldrums. Still, some analysts have continued to voice concern about the market’s dependence on AI, as tech firms face increased pressure to turn massive capital investment into profits.

Analysts say that 2026 could shape up to be yet another big one for stock investors. Although, with leadership changes at the US central bank and mounting concerns that AI stocks are overvalued, the path ahead might be bumpy. Expectations for lower borrowing costs could be an additional catalyst for corporate earnings in 2026 and drive stock prices higher. Strong earnings growth in corporate America has been a key driver of the stock market rally since the tariff-driven whiplash in the spring. At the same time, geopolitical tensions, Trump’s tariffs and expectations of interest rate cuts added to investor demand this year for safe haven assets, such as gold and other commodities. The price of gold was up by about 70% during 2025.

But 2026 will contain a number of major economic question marks including Trump’s tariff policies and the resulting negotiations with major trading partners along with Trump’s expected announcement of a new Federal Reserve chairmen in the coming weeks. Trump, who has been pressuring current Federal Reserve chairman Powell to lower interest rates, has said he will pick a Fed chair who he views as committed to easing borrowing costs. Wall Street investors will be focused on understanding how the change in leadership will impact monetary policy moving forward.

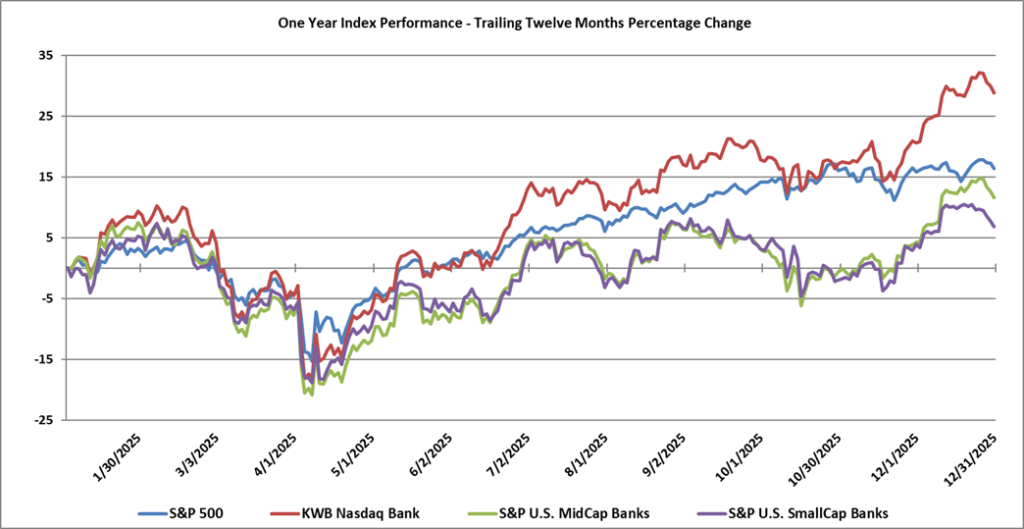

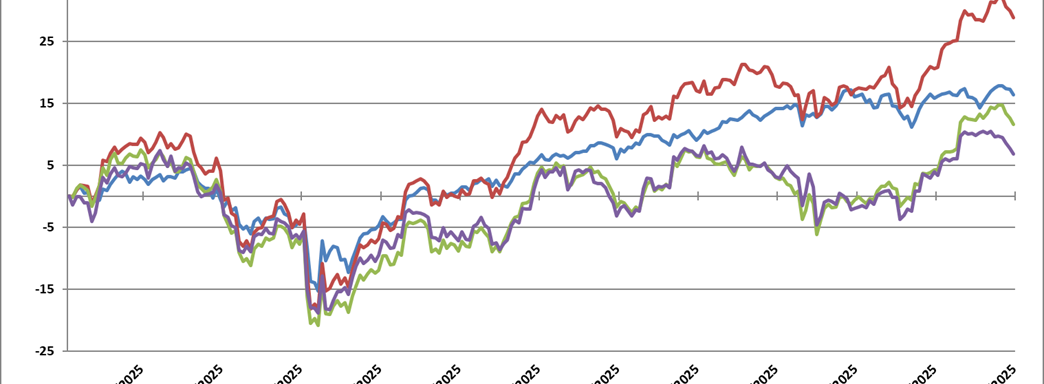

Bank stocks, although volatile at times, rallied higher for most of the fourth quarter but softened late in December, generally matching the movements for the broader market in the fourth quarter. Bank stocks ended in positive territory during 2025, although softening during December. The KBW Nasdaq Bank Index posted a 7.7% increase during the fourth quarter of 2025 (down by 2.6% during the last week of the year) compared with a rise of 9.2% in the third quarter of 2025. This index was up by 62.8% over the past three-year period. By comparison, smaller banks posted lower returns during the fourth quarter of 2025, with the S&P U.S. SmallCap Bank index increasing by 2.9% in the quarter (down by 3.6% during the last week of December) with the index being up by 6.8% during the past year while posting a three-year rise of 18.9%. The S&P U.S. MidCap Bank index increased by 7.5% during the fourth quarter of 2025 (down by about 3% in last week of December) compared to the increase of 4.6% during the third quarter of 2025 leaving it up by 11.6% over the past year, and up by a modest 1.6% over the past three years. By comparison, the S&P 500 was up by 2.4% during the fourth quarter of 2025 leaving it up by 16.4% during the past year. The S&P 500 was up by approximately 78.3% during the past three-year period compared to the 62.8% increase for the KBW Nasdaq Bank Index and the 122.1% increase in the technology heavy Nasdaq. The Nasdaq increased by 2.6% during the fourth quarter of 2025 and was up by 20.4% for the full-year 2025.